Many company directors assume HMRC only opens HMRC enquiries when it has already found a mistake. In reality, HMRC investigations can begin through several channels, including random selection, sector-wide compliance campaigns, and risk profiling based on statistical analysis.

Even fully compliant businesses may still receive HMRC enquiries, particularly in industries HMRC considers higher-risk or where director remuneration structures are more complex.

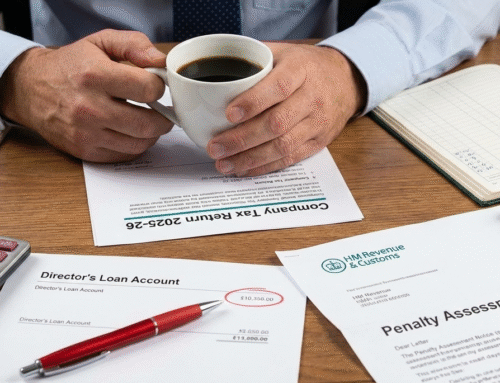

Why HMRC Opens HMRC Enquiries into Directors

HMRC does not only investigate when an error is confirmed. Enquiries may start because:

- A business has been selected at random

- HMRC is running a sector-specific compliance campaign

- Statistical risk models flag certain patterns as higher-risk

Directors operating in industries with frequent self-employment issues or known avoidance schemes are more likely to face enquiries, even when no wrongdoing has occurred.

Common Focus Areas for Director Enquiries

HMRC is expected to concentrate on the following areas throughout 2026:

- Director remuneration and dividend planning

- Overdrawn director’s loan accounts

- Personal use of company assets

- Expense claims with mixed personal and business use

These areas receive attention because mistakes are common and can lead to underpaid taxes.

How Enquiries Escalate

The outcome of an enquiry often depends on how a director responds.

Late submissions, unclear explanations, or unprofessional communication during HMRC enquiries can prompt HMRC to widen the scope of its investigation.

In many cases, a single enquiry can expand into a review of multiple tax years if HMRC believes information is missing or inconsistent.

How Directors Should Respond

All HMRC correspondence should be treated as official and urgent.

Directors should respond promptly with accurate information supported by clear documentation.

Early engagement helps prevent routine checks from escalating and reduces the disruption and stress that prolonged enquiries can create.

The Impact on Directors

Even when no additional tax is due, enquiries require time, resources, and attention from businesses.

Directors who understand why HMRC opens enquiries are better positioned to respond strategically and protect both business operations and personal standing.

Take Action Today

HMRC enquiries aren’t always a sign of wrongdoing, but how you respond can prevent a routine check from escalating. Review your director’s loan accounts, dividend records, and expense documentation now. If you’re unsure about anything, contact one of our advisors for a director compliance review today to stay fully prepared.

FAQs

- Why would HMRC open an enquiry if my business is fully compliant?

HMRC initiates enquiries through multiple channels, not only when errors are suspected. These include random selection, sector-specific compliance campaigns, and risk profiling. Even compliant directors may be contacted as part of routine compliance activity.

- What areas is HMRC focusing on in 2026 director enquiries?

Key focus areas include director remuneration and dividend planning, overdrawn director’s loan accounts, personal use of company assets, and expense claims with mixed business and personal use.

- How can I prevent an initial enquiry from escalating?

Respond promptly and professionally. Provide documentation-backed answers within agreed timeframes. Late or vague responses often trigger wider investigations across multiple tax years.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}